Language learning in Germany

A market survey conducted in November and December 2023 reveals a society that is very busy with language learning. The DCMN Brand Tracker surveyed 2000 German consumers, with 61 percent indicating they have learned at least one foreign language at some point. A further 16 percent were actively engaged in language learning at the time of the survey, and another 14 percent planned to start learning a new language in the near future. Taken together, this means that nearly a third of Germans were either studying a language at the time or intend to do so.¹

Newer market reports, such as that commissioned by Spherical Insights, suggest that this is not a short-lived post-pandemic bubble. Analyses of Germany’s online language learning platform market show strong, ongoing growth, with digital offerings expanding at a high double-digit compound annual rate. These studies highlight Germany as one of Europe’s more dynamic online language learning markets, driven by a combination of personal, academic, and professional demand, rather than a single, narrow use case.²

Price is the top decision factor for 73% of German learners, followed closely by quality of materials (61%) and flexibility (59%).

“Lost in Translation: Language Learning in Germany.” DCMN Blog – The Marketing Hub, January 15, 2024.

Why are Germans learning languages?

When Germans decide to learn a language, travel is still the number one trigger. In the DCMN study, 55 percent of respondents cited travel as their primary motivation, underlining the practical value of being able to navigate hotels, restaurants, and real-life situations abroad. Self-development came a close second at 45 percent, reflecting a widespread belief that languages sharpen the mind, broaden horizons, and contribute to a sense of personal growth. Cultural understanding (37 percent) and personal relationships (33 percent) ranked next, pointing to the emotional and social dimensions of language learning: connecting with partners, family members, and friends, or engaging more deeply with films, books, and music.¹

More recent German and European market analyses echo these basic themes. Reports on the online language learning platform segment describe a demand mix in which personal development, career advancement, and travel all play key roles. Europe-focused industry overviews emphasize that languages are not just a school requirement but a tool for international careers, Erasmus-style mobility, and cross-border work in multinational companies.² ³

Germany ranks 10th globally in the EF English Proficiency Index 2025, in the “high proficiency” band with a score of 598/800, meaning many learners are already intermediate or advanced.

EF Education First. 2025. EF English Proficiency Index 2025. Zurich: EF Education First.

How can you segment the language training market in Germany?

One of the most striking aspects of the current German language learning landscape is the age profile of active learners. DCMN’s data highlight particularly high activity among 30–35-year-olds, situating language learning squarely in the early-to-mid-career life stage, rather than only in classrooms or universities. This is the phase when many professionals change jobs, relocate to other countries, or assume roles that require more international communication, and the survey suggests they are willing to invest in language skills to support these transitions.¹

Spherical Insights reports on online language learning platforms in Germany. They show that individual adult learners, rather than institutional buyers alone, make up the largest and fastest-growing share of revenue. Their report describes “digital self-tutoring” as a core growth engine: self-paced, direct-to-consumer online offerings purchased by individuals for their own upskilling, often in conjunction with work and family commitments.²

Digital Learning in Germany

If you picture language learning in Germany as old-fashioned, it is time to update that image. In the DCMN Brand Tracker, 59 percent of respondents reported a preference for learning via language apps, making apps the most popular format. Online private lessons (34 percent) and online group courses (25 percent) were also frequently mentioned, whereas physical group courses (21 percent) and physical private lessons (19 percent) ranked lower. The hierarchy here is clear: flexibility and convenience beat physical proximity for many learners.¹ The market has gravitated towards online solutions.

The broader market data illustrate the extent of this digital shift. A 2024 report on Germany’s online language learning platform market identifies digital self-tutoring as the leading revenue segment. It expects it to maintain the highest growth rate in the coming years.² Complementary global app statistics reveal that language learning apps generate billions of dollars in revenue worldwide, with mobile-first, self-paced learning dominating usage patterns.⁴ In other words, the German preference for app-based learning sits within the global shift from fixed-schedule classes toward “learning on the go” on a smartphone.

Which languages are Germans learning?

Germany’s digital learners are not splitting their attention equally across all languages. In the DCMN study, English, Spanish, and French clearly emerged as the primary languages of interest among app users. English remains the default choice for international communication and professional mobility, while Spanish and French combine work relevance with strong cultural and travel appeal. Notably, the survey highlighted Spanish as a rising star, with 27 percent of respondents planning to learn it in the future.¹

Language‑segment analyses of the German online learning market broadly confirm this pattern. English accounts for the largest share of platform revenues and learner numbers, reflecting its status as the global language of business, research, and higher education. At the same time, Spanish and French are among the key growth languages, supported by tourism, the Erasmus mobility program, and a growing interest in European and Latin American culture.² ³ For providers, this means that English remains non-negotiable, but Spanish in particular offers significant room for expansion.

What app brands are shaping the market?

When Germans reach for an app to learn a language, a small cluster of brands dominates their screens. In DCMN’s 2023 Brand Tracker, Babbel stood out as the most recognized and most used language learning app in Germany, with 71 percent of respondents recognizing the brand and 51 percent reporting having tried it. Duolingo followed in second place, with 49 percent awareness and 44 percent usage. Rosetta Stone, Busuu, Tandem, and Lingoda also appeared in the ranking, each offering a slightly different value proposition, from AI-powered lessons to live virtual classrooms or language exchange with native speakers.¹

More recent digital analytics show that these leading brands have not lost their grip on German learners’ attention. Sensor Tower’s 2024 Q3 analysis of Germany’s education and training apps finds Duolingo and Babbel at the top in terms of web visits and app engagement.⁵ At the same time, a 2023 Statista study of aided brand awareness in Germany again places Babbel at the head of the league table for language learning apps, with Duolingo, Busuu, and others following.⁶ These newer data sets do not repeat DCMN’s exact percentages, but they corroborate the overall picture: Germans are highly aware of Babbel and Duolingo, and they use them heavily. Some of the best-known language learning app providers in Germany are:

- Babbel

- Duolingo

- Busuu

- Rosetta Stone

- Lingoda

What Germans look for in a language app

Of course, awareness alone does not guarantee subscriptions. In the DCMN survey, Germans interested in language learning ranked price as the top decision factor when choosing an app or platform, with 73 percent naming it a priority. Quality of course materials (61 percent) and flexibility (59 percent) followed closely, indicating that learners want a combination of pedagogical substance and the freedom to learn at their own pace and in their preferred learning environment. Creativity and innovation, including gamified features, were valued by 39 percent of respondents, underscoring the importance of engaging and varied content.¹

Broader app‑market statistics provide some context for these preferences. Global analyses of language learning apps reveal that mobile, self-paced products dominate revenue, indicating that the price–value equation is being evaluated in a highly competitive, subscription-driven environment.⁴ In practical terms, this means German learners are likely to choose platforms that balance transparent, affordable pricing with strong content design, intuitive UX, and flexible micro‑learning formats.

What does this mean for the future of language learning in Germany?

Taken together, these data points reveal a language learning ecosystem in Germany that is both mature and still evolving. A majority of adults already have some foreign language experience, and a significant share is learning now or planning to start. App-based, self-directed learning has moved from the edges to the center, with digital self-tutoring emerging as the dominant business model. English remains the foundation, but Spanish and French and, increasingly, other languages, are carving out growth niches, especially among travel‑ and culture-motivated learners.

For educators, instructional designers, and edtech providers, the message is clear. In Germany, language learning is no longer confined to evening classes and school timetables. It is something adults slot between meetings on the S‑Bahn, on their lunch breaks, or late in the evening on the sofa, with expectations shaped by consumer apps in other domains. Meeting those expectations will mean combining solid pedagogy, thoughtful content design, and intelligent use of technology with a pricing and delivery model that fits seamlessly into busy, highly mobile lives.

How big is the corporate training market?

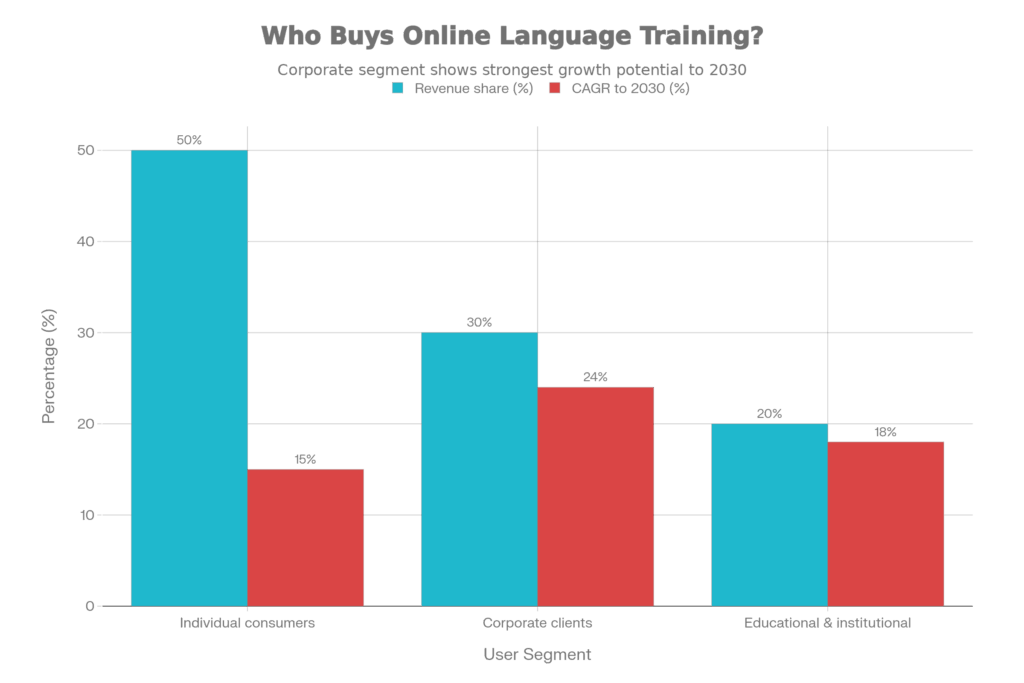

Corporate demand is becoming one of the main engines of the online language learning market, and Germany is firmly part of that shift. Segment analyses of the global online language learning market show that while individual consumers still generate the largest share of revenue by volume, corporate clients are the fastest-growing end-user group, expanding at around 24–25 percent CAGR (Compound Annual Growth Rate) to 2030, driven by bulk licenses, analytics dashboards, and single‑sign-on integrations that fit into existing HR tech stacks.⁷ In practice, many multinationals operating in or from Germany now frame language training not only as a sales and mobility enabler, but also as part of their ESG and DEI agendas, ensuring that employees across locations have equitable access to English and local language skills.⁷ ⁸

Across major market reports, corporate and institutional customers already account for roughly half of global online language-learning revenue, with corporate learners singled out as a premium ARPU segment due to higher per-seat pricing and multi-year contracts.⁷ ⁸ ⁹ This means a growing share of the world’s English lessons, and a significant chunk of business‑focused German, now happens on enterprise platforms commissioned by L&D and HR teams, with detailed usage and outcome data feeding back into learning analytics and talent dashboards rather than sitting in stand‑alone consumer apps.⁷ ⁹

What are the high-potential areas in the German market?

AI‑powered speaking practice

Speaking remains the weakest and most anxiety-inducing skill for many non‑native users of English and other foreign languages, even when their reading and listening are relatively strong.¹² This creates a clear opportunity for AI-driven oral practice tools that simulate real conversations, provide instant feedback on pronunciation and pragmatics, and help learners rehearse high-stakes situations (presentations, interviews, client calls) in low-risk environments.¹² Potential offerings include voice-enabled AI tutors with context-aware feedback, German‑localized chatbots that understand workplace scenarios, or VR/AR role-play environments that train users to “speak confidently in real situations” without needing to schedule a teacher-led lesson.¹² ¹⁴

Segmented content for corporate and niche English

Generic “general English” apps leave many German professionals under‑served, especially in regulated or technical fields. Market reports on Europe’s online language learning and English‑teaching sectors highlight growing demand for industry-specific and role-specific English, such as medical, legal, engineering, or finance English, as well as German for expatriates and cross-border workers.¹⁰ ¹⁵ Tailored B2B solutions that plug into corporate LMS and HRIS systems, offering Medical English for hospital staff, English for finance and controlling, or English for supply‑chain teams, address clear jobs‑to‑be‑done and can command higher ARPU than mass‑market courses.¹⁰ ¹⁵ Similarly, exam-oriented segments (TOEFL/IELTS prep) and tourism‑industry English remain relatively under‑served by generalist apps and could be bundled with analytics that show HR and universities tangible progress data.¹⁰

Youth and education integration

Across Europe, the under-18 age group is the single largest and often fastest-growing segment in online language learning by revenue share and growth rate.¹⁵ ¹⁶ Meticulous Research expects under-18s to dominate the European online language learning market from the mid-2020s onward, driven by demand for interactive, gamified experiences and the growing importance of multilingual skills for mobility and careers.¹⁵ In Germany, this aligns with DigitalPakt-funded school digitization: partnerships with schools, publishers, or Länder authorities that offer curriculum-aligned English support, AR/VR “immersive” modules, and after-school or Feriencamp add-ons could capture a large youth user base while satisfying local curricular and data protection constraints.¹¹ ¹⁷

Hybrid and blended models

Evidence from German consumer surveys and European market forecasts suggests a strong preference for self-paced apps complemented by human feedback, rather than purely self-study or classroom-based models.¹ ¹⁵ Providers like Lingoda already combine live CEFR-aligned classes with self-study materials, while Busuu layers community feedback and AI tools onto app-based study.¹⁸ For new entrants, blended offerings could differentiate through micro‑coaching (short, focused live sessions), employer or insurer partnerships, micro‑scholarships, or subscription bundles that keep costs manageable for price-sensitive Germans, 73 percent of whom cite price as their top factor when choosing a language app.¹

Accessibility and affordability

Price sensitivity and equity concerns create space for freemium and subsidized models that broaden access beyond affluent urban professionals.¹ ¹⁰ Public and private stakeholders in Germany are investing heavily in AI and digital education, including for integration, vocational training, and upskilling of migrants and low‑income groups.¹¹ An appealing model could be an “English‑learning passport” integrated into Berufsschule, Ausbildung, or integration courses, with costs partially covered by government schemes or employers; such a model recognizes that, alongside German, English language skills substantially improve access to global labour markets and remote work opportunities.¹⁰ ¹⁵ For founders and investors, these inclusion-oriented designs are not only socially valuable but also align with ESG mandates and can unlock public co-funding or impact‑investment capital.¹¹ ¹⁹

Strategic implications for investors

Given the high presence of established players, scale and differentiation are non‑negotiable for new entrants. Babbel enjoys around 71 percent brand awareness in Germany, with Duolingo close behind at roughly 49 percent. This means any new app will have to fight for attention against two strongly entrenched brands with substantial marketing muscle.¹ To build a viable position, investors should back models that offer clear differentiation, whether through unique technology (for example, AI‑driven conversation partners and speaking feedback), a defensible content niche (such as industry‑specific English or German for specific professions), or strategic partnerships with schools, universities, corporate L&D, and public agencies.¹ ⁷ Emphasis on blended or highly personalised offerings, self‑paced content combined with live coaching, mentoring, or adaptive pathways, can create niches where completion rates, skill gains, and perceived value clearly exceed those of generic apps.⁷ ¹⁰

Regulation and data governance are equally central to investment decisions. Any EdTech operating in Germany must comply with GDPR, the German Federal Data Protection Act, and the EU AI Act, which together impose strict requirements on transparency, risk management, human oversight, and privacy‑by‑design for AI systems used in education and training.¹¹ ²¹ Trade and government guidance explicitly stress data protection by design and responsible AI as preconditions for large‑scale deployments in schools and universities.¹¹ ²¹ For startups working with speech data, behavioural analytics, or biometric‑style signals (such as voice), robust data‑governance frameworks and clear documentation of models, data flows, and DPIAs are no longer optional. They are key to winning trust from institutional buyers and passing future audits.¹¹

Revenue models and go‑to‑market strategies need to reflect both German price sensitivity and the mixed B2C/B2B nature of the market. In the DCMN survey, 73 percent of German language learners named price as their top decision factor, ahead of quality and flexibility, underscoring that even digitally savvy users are highly cost‑conscious.¹ In this context, hybrid monetisation, combining reasonably priced subscriptions, enterprise or institutional licences, and potentially freemium tiers or ad‑supported options may perform better than a single, rigid model.⁷ ⁸ Following the trajectory of B2B‑oriented providers such as Speexx and Learnlight, an enterprise‑first approach that integrates with existing LMS and HR systems, offers robust analytics, and sells into HR/L&D budgets can create more predictable revenue and referral loops. At the same time, consumer offerings build brand recognition in parallel.⁷ ⁸ ¹³ ¹⁴ Co-investment or pilots with government and educational bodies, particularly in areas aligned with DigitalPakt Schule or AI‑in‑education priorities, can open subsidised channels and reduce customer‑acquisition costs.¹¹ ¹⁷

Finally, technological edge remains a decisive factor, but it must be deployed strategically. Market analyses consistently identify AI (adaptive learning, conversational agents, predictive analytics) and immersive technologies (AR/VR) as central growth drivers in online and mobile language learning, with mobile‑first self‑learning accounting for the majority of usage and revenue.⁷ ¹⁴ ²² For investors, this suggests prioritising platforms that are mobile‑first, cross‑device, and capable of using AI to personalise content and feedback while keeping R&D costs and compliance burdens manageable.⁷ ¹⁴ Rather than funding AI features for their own sake, capital should focus on capabilities that produce measurable ROI, such as demonstrable gains in speaking proficiency or exam performance, and that can be clearly communicated to learners, institutions, and regulators.¹¹ ¹⁴

Risks and barriers

Despite favourable fundamentals, there are several risks and structural barriers that investors need to weigh. The first is market saturation and competition. The consumer language‑app space is crowded with global brands, regional players, and offline institutions offering digital extensions. Customer switching costs remain low.⁷ ⁴ As Babbel and Duolingo dominate brand awareness and app‑store rankings in Germany, any new entrant must spend heavily on marketing and user acquisition or find highly targeted niches to reach sustainable CAC/LTV ratios.¹ ⁵ Investors should closely examine acquisition strategies, organic growth levers, and whether a startup’s proposition is sufficiently distinctive to stand out in a noisy market.⁷ ⁸

A high English‑proficiency baseline also raises the bar for perceived value. Germany ranks 10th globally in EF’s 2025 English Proficiency Index, sitting in the ‘high proficiency’ band with a score of 598 out of 800 20 In this context, generic beginner content risks being seen as “nice‑to‑have” rather than essential; offerings must address concrete gaps, such as advanced speaking fluency, specialised workplace vocabulary, writing for professional contexts, or exam preparation, espeically if they are to command meaningful willingness to pay and sustained engagement.¹⁰ ¹²

Cultural and institutional adoption is another challenge. Although Germany has invested heavily in digital infrastructure and AI‑in‑education initiatives, parts of the school and higher‑education sectors remain cautious about commercial apps and AI in the classroom.¹¹ ¹⁷ Some teachers, parents, and unions still prefer in‑person or traditional instruction, and curriculum integration can be slow without official endorsement or alignment with state‑level standards.¹¹ ¹⁹ Building credibility through academic partnerships, independent effectiveness studies, recognised certifications, and clear curricular mapping is therefore essential, especially for solutions targeting the K–12 and HE segments.¹¹

Economic and funding risks also need to be taken into account. Since the pandemic‑era boom, global EdTech valuations have cooled, and later-stage funding has become more selective, even as German EdTech investment volumes rebounded sharply in 2025.¹⁸ ¹⁹ Startups that rely on successive growth‑equity rounds need a credible path to profitability or clear strategic exit options, as illustrated by Learnlight’s 2017 growth‑equity deal and subsequent private‑equity ownership.¹³ ¹⁴ Macro‑economic uncertainty, changing interest rates, and shifting public budgets for education can all dampen purchasing cycles and valuations, particularly for discretionary B2C products.¹⁸

Finally, data and AI ethics pose both regulatory and reputational risks. Beyond the hard requirements of the AI Act and GDPR, learners, parents, and institutions are increasingly wary of opaque AI systems and aggressive data‑collection practices.¹¹ ²⁰ EF’s 2025 English Proficiency Index and related commentary highlight the importance of “responsible AI” in language learning, stressing transparency, explainability, and demonstrable learning outcomes rather than hype.¹² ²⁰ Overstating AI capabilities or failing to show real educational benefit can quickly undermine trust and invite public scrutiny.¹¹ ²⁰ For investors, this makes ethical and explainable AI a core due‑diligence criterion rather than an optional extra, especially in a highly regulated, reputation-sensitive market like Germany.¹¹ ²⁰

What this means for language trainers

For language trainers, this evolving landscape in Germany is both a challenge and a significant opportunity. Instead of competing head‑on with apps, trainers who position themselves as designers of learning experiences, combining high‑quality human interaction with digital tools, are likely to be in greatest demand.

First, there is clear space for trainers to specialise. Corporate and institutional buyers increasingly seek industry‑specific and role‑specific language skills (for example, Business English for finance, German for engineers, medical communication, or exam preparation), which generalist apps rarely cover well.¹⁰ ² Tailored programmes that connect tightly to workplace tasks, KPI frameworks, and talent strategies can command higher rates than generic “conversation classes” and align neatly with the B2B growth described in online language learning market reports.⁷ ⁸ ² Trainers who can speak the language of HR and L&D, learning objectives, ROI, analytics etc. , will be better positioned to win corporate contracts or freelance mandate work.⁷ ⁸

Second, digital and hybrid competence is becoming central to the trainer profile in Germany. Adult learners and companies alike are gravitating toward self‑paced and app‑supported formats complemented by live coaching, which means trainers who are comfortable running online group sessions, 1:1 virtual coaching, and blended learning models can plug directly into platforms like Lingoda, Speexx, or corporate LMS environments.¹ ¹⁸ ⁷ Trainers who can design short, focused, high‑impact sessions that sit around an app‑based core (for example, 30‑minute micro‑coaching calls on speaking or feedback on recorded tasks) will fit especially well into the “digital self‑tutoring plus human support” models German companies are buying.² ⁷

Third, the rise of AI does not remove trainers from the equation; it changes what they are paid for. AI tools can already handle many drill‑type activities and basic corrective feedback, particularly in receptive skills and simple speaking practice, but they struggle with nuanced pragmatic choices, intercultural communication, complex writing, and affective support.¹² ²¹ Trainers who learn to orchestrate AI tools—using them for scalable practice and diagnostics while focusing their own time on higher‑order skills, coaching, and personalised guidance—will be more valuable to both learners and employers.¹¹ ²¹ National and European initiatives on AI in education emphasise “responsible AI” and teacher‑in‑the‑loop models, which means trainers who understand these frameworks can also contribute to policy‑compliant course and tool design.¹¹ ²¹ ²³

Finally, language trainers who engage with the youth and integration segments will find a growing, if complex, field. Under‑18s and learners in vocational and integration pathways are among the fastest‑growing groups in online language learning, and German public investment via DigitalPakt Schule and other programmes is gradually improving infrastructure and openness to digital tools.¹⁵ ¹⁷ At the same time, these contexts carry higher regulatory and ethical expectations: child protection, accessibility, inclusion, and alignment with formal curricula.¹¹ ¹⁷ Trainers who can design or deliver curriculum‑aligned, inclusive programmes that blend classroom and digital components—whether for school English, Berufsschule English, or German for migrants—will be well‑placed to work with schools, Träger, and public‑private partnerships.¹¹ ¹⁷ ¹⁹

For individual freelancers and in‑house trainers, the practical implications are clear: specialise rather than generalise, learn to work fluently with digital platforms and AI tools, and build credibility with corporate and institutional stakeholders by speaking their language of outcomes, compliance, and learner analytics. Those who do so will not be replaced by EdTech; they will be the ones making EdTech truly effective in the German language learning ecosystem.⁷ ⁸ ¹¹ ²¹

Conclusion: A Maturing Market at an Inflection Point

Germany’s language learning market stands at a pivotal moment. Consumer demand remains robust and the market has decisively shifted from classroom-based instruction to digital-first, self-paced models that fit busy, mobile lives. Within this landscape, corporate demand is accelerating faster than consumer adoption, with enterprises investing in language and cross-cultural communication as core talent and mobility tools. For investors, the opportunity is real but requires strategic differentiation: blended models, niche content, strong data governance, and B2B go-to-market strategies outperform me-too consumer apps. For language trainers, the trajectory is clear: those who position themselves as learning designers, integrators of AI and digital tools, and strategists for talent and compliance will thrive; those clinging to traditional delivery models risk obsolescence.

The data converge on a simple insight: language learning in Germany is neither contracting nor consolidating under dominant players alone. Instead, it is fragmenting into multiple parallel streams—generalist consumer apps (Babbel, Duolingo) serving price-sensitive self-learners; specialized B2B platforms (Speexx, Learnlight, corporate LMS integrations) serving enterprises; niche offerings serving underserved sectors (medical, legal, finance, tourism); youth and integration initiatives supported by public funding; and hybrid blended models combining self-study with micro-coaching or live classes. This segmentation creates openings for new entrants and for trainers who understand their local market, regulatory environment, and learner needs.

For the next five years, three macro trends will shape the competitive landscape: first, deepening integration of AI into every segment, with emphasis on responsible, explainable systems; second, tightening regulatory requirements (EU AI Act, GDPR, data protection) that will deter low-governance startups but reward well-designed, compliant solutions; and third, a growing emphasis on measurable outcomes and skill certification, driven by HR/L&D buyers who demand evidence of learning impact, not just engagement metrics. Founders, investors, educators, and trainers who align with these trends, and who understand the specific cultural, economic, and institutional context of Germany, will find a mature, lucrative, and dynamic market ready to reward innovation and integrity.

ChatGPT Deep Research was used to help compile this report. The information contained in the article is from various websites. I do not take any responsibility for the accuracy of this.

The image is AI-generated

References

- Bocian, Monika. 2024. “Lost in Translation: Language Learning in Germany.” DCMN Blog – The Marketing Hub, January 15, 2024. https://blog.dcmn.com/language-learning-in-germany/.

- Spherical Insights. 2024. Germany Online Language Learning Platform Market Size, Price. December 31, 2024. https://www.sphericalinsights.com/reports/germany-online-language-learning-platform-market.

- eLearning Journal. 2020. “Europe’s Digital Language Learning Market Is Growing Strongly.” eLearning Journal, January 20, 2020. https://www.elearning-journal.com/en/2020/01/21/europes-digital-language-learning-market-is-growing-strongly/.

- ElectroIQ. 2025. “Language Learning App Statistics by Revenue and Facts (2025).” ElectroIQ, November 26, 2025. https://electroiq.com/stats/language-learning-app-statistics/.

- Sensor Tower. 2024. “Leading Brands in Germany’s Education & Training Sector, Q3 2024.” Sensor Tower Blog, December 31, 2024. https://sensortower.com/blog/2024-q3-de-leading-3-Education—Training-brands.

- Statista. 2024. “Top Language Learning Apps in Germany in 2023, by Aided Brand Awareness.” Statista, September 10, 2024. https://www.statista.com/statistics/1490109/language-learning-app-awareness-germany/.

- Mordor Intelligence. 2025. Online Language Learning Market – Size, Share, and Industry Analysis. Hyderabad: Mordor Intelligence. https://www.mordorintelligence.com/industry-reports/online-language-learning-market.

- Meticulous Research. 2023. Online Language Learning Market by Product, Mode, and End User – Global Forecast to 2031. Pune: Meticulous Market Research Pvt. Ltd. https://www.meticulousresearch.com/product/online-language-learning-market-5025.

- Cognitive Market Research. 2025. Online Language Learning Market Report 2023–2030. Indore: Cognitive Market Research. https://www.cognitivemarketresearch.com/online-language-learning-market-report.

- Meticulous Research. 2024. Europe Online Language Learning Market by Size, Share, Forecasts to 2032. Pune: Meticulous Market Research Pvt. Ltd. https://www.meticulousresearch.com/product/europe-online-language-learning-market-5549.

- International Trade Administration. 2024. “Germany AI in Education.” Market Intelligence – U.S. Department of Commerce, November 18, 2024. https://www.trade.gov/market-intelligence/germany-ai-education.

- Grunwald, Eric. 2024. “Non‑Native English‑Speaking Graduate Students Still Face Significant Disadvantages.” MIT Faculty Newsletter 36, no. 5 (May–June). https://fnl.mit.edu/may-june-2024/non-native-english-speaking-graduate-students-still-face-significant-disadvantages/.

- Learnlight. 2017. “Learnlight Receives Major Growth Equity Investment from Beech Tree Private Equity.” Learnlight News, April 3, 2017. https://www.learnlight.com/en/articles/learnlight-receives-major-growth-equity-beech-tree/.

- Kings Research. 2025. Online Language Learning Market Size Report, 2030. Dubai: Kings Research. https://www.kingsresearch.com/online-language-learning-market-41.

- Meticulous Research. 2023. Language Learning Market by Age Group (<18 Years, 18–20 Years, 21–30 Years, 31–40 Years, >40 Years) and Language – Global Forecast to 2030. Pune: Meticulous Market Research Pvt. Ltd. https://www.meticulousresearch.com/product/language-learning-market-5561.

- Grand View Research. 2024. Europe Online Language Learning Market Size & Outlook to 2030. San Francisco: Grand View Research. https://www.grandviewresearch.com/horizon/outlook/online-language-learning-market/europe.

- Bundesministerium für Bildung und Forschung. 2025. “DigitalPakt Schule.” BMBF, March 25, 2025. https://www.bmftr.bund.de/DE/Bildung/Schule/Digitalisierung/DigitalpaktSchule/digitalpaktschule_node.html.

- Lingoda. 2025. “Lingoda vs. Busuu: Head‑to‑Head Comparison.” Lingoda Blog, November 19, 2025. https://www.lingoda.com/blog/en/lingoda-vs-busuu/.

- Research and Markets. 2024. EdTech in Germany: Market Summary, Competitive Analysis and Forecast, 2020–2028. Dublin: Research and Markets. https://www.researchandmarkets.com/reports/5973512/edtech-in-germany.

- EF Education First. 2025. EF English Proficiency Index 2025. Zurich: EF Education First. https://www.ef.com/epi/.

- EF Education First. 2025. “EF English Proficiency Index 2025 Launched: AI‑Powered Insights Reveal New Speaking and Writing Gaps.” EF Press Room, November 24, 2025. https://www.ef.com/wwen/about-us/press/articles/2025/ef-english-proficiency-index-2025-launched/.

- Industry Research. 2024. Online Language Learning System Market Size – Global Report to 2034. London: Industry Research. https://www.industryresearch.biz/market-reports/online-language-learning-system-market-112165.

Comments are closed